AI in Real Estate: How One Real Estate Agent Empowers Clients

AI in real estate is getting hot. AI is the talk of the town lately in every sports bar, every...

AI in real estate is getting hot. AI is the talk of the town lately in every sports bar, every...

Generate a Comparative Market Analysis You can now get a CMA or Comparative Market Analysis of a home without any...

The Northwest Multiple Listing Service (NWMLS) and the Olympic Listing Service (OLS) are two competing MLS providers serving the real...

Selling a home, buying a new one, and transitioning between the two can be an challenging process and nearly all...

A new Sequim Real Estate Community online is now available for buyers who are planning to move to the Sequim...

“The good news is that recessions often act as catalysts for innovation.” Carmine Gallo, The Innovation Secrets of Steve Jobs...

There was a radio host who used to say, "I'm having more fun than a human being is entitled to...

I'm extremely excited to share big news from iRealty Virtual Brokers. The news is that I just did a massive...

Is Sequim always sunny? The direct answer is absolutely no. But that does't mean the Sequim Blue Hole isn't real....

Is there really a Sequim Real Estate Trilogy? Yes there is. It's not a fictional trilogy like Lord of the...

There is a tectonic shift happening under our feet right now, and that is the huge move from the big...

Covid-19 continues to impact the Sequim real estate market for buyers and sellers, and of course, for Realtors, escrow companies,...

Yesterday I wrote about how homes in the Sequim area are selling fast and faster. Today I am taking this...

Sequim videos for buyers just got organized. If you're a retiree or soon to be, and you're looking closely at...

How do you Find Your Home in Sequim? If you're a buyer in a state other than Washington, and you're...

Introduction to 5 Installments: Selling your home is no small matter, and since I've been in the real estate business...

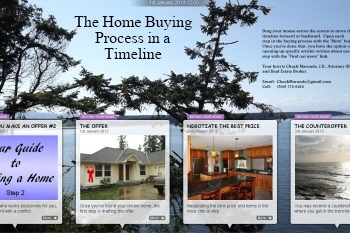

The home buying process can be laid out in an orderly timeline. I created a visual aide that lays the...

The largest Sequim Real Estate Blog just got a massive upgrade, and as a buyer, we think you're going to...

The largest real estate blog in Sequim for ten years and running is still Sequim-Real-Estate-Blog.com or simply SequimBlog.com. We just...

This Sequim mobile app is a very powerful smartphone tool whether you use an Android or an iPhone, and you...

"I wish I read this before selling my

home. I could have saved $50,000." Andy

The largest independent real estate blog in the State of Washington with over 2,200 articles totally focused on our client’s best interest, their needs and their curiosity. All free and 100% reliable. I’m here if you need me,