What happens if get a low appraisal that comes in below your purchase price? This could turn into a nightmare scenario, but there is a seasoned approach to handling a low appraisal. First, we’ll look at the immediate consequences, and then we’ll look at the solutions.

What a Low Appraisal Means

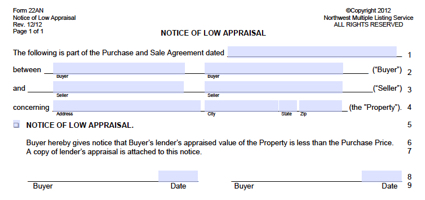

It does not happen very often, but once in a great while a low appraisal comes in below the purchase price. When that happens, the contract language provides options for the buyer and seller. Upon receiving a low appraisal, the buyer issues a Notice of Low Appraisal to the seller. The Notice of Low Appraisal presents the seller with three options:

Option 1: Seller hereby gives notice that a reappraisal or reconsideration of value has been completed in an amount not less than the Purchase Price. Buyer shall promptly seek lender’s approval of the reappraised or reconsideration of value.

Option 2: Seller hereby consents to reduce the Purchase Price to $______ (an amount not more than the amount specified in the appraisal or reappraisal by the original appraiser, or an appraisal by another appraiser acceptable to Buyer’s lender, whichever is higher).

Option 3: Seller hereby gives notice that Seller rejects Buyer’s notice of low appraiser and (1) will not cause a reappraisal or reconsideration of value to be completed; and (2) does not consent to a reduction of the Purchase Price.

Overcoming a Low Appraisal

While these look like logical options for a seller, and they are, there really is only one practical option for a seller in this real estate market: lower the price to match the low appraisal value. Why is this the only practical option?

I represented a buyer in the purchase of their home in Sequim, and the appraisal came in $30,000 less than the agreed price, which was just under $400,000. That was a surprise to all of us. The sellers were quite disappointed naturally, but here’s why their only practical remedy was to accept the lower price.

The buyer’s lender will only extend a loan based on the loan to value ratio (i.e. 80%) of the purchase price or the appraisal value, whichever is lower. The only way a buyer could pay a higher price above the appraised value is if the buyer came up with the additional cash for the difference. In this case, the buyer would have to come up with their 20% down payment of the appraised value plus an additional $30,000 in cash to make up the difference. That simply doesn’t work for most buyers, and buyers would generally be adverse to paying more than the appraised value anyway.

If a seller chooses the reappraisal option, the entire closing will have to be extended for weeks to have time for another appraiser to come in and then what do you get? You get a second appraisal that probably comes in fairly close to the first appraisal since they are using the same sales comps and replacement costs in their evaluation. If the second appraisal comes in higher, you would still have the challenge of getting the buyer’s lender (the underwriter) to accept the second appraisal, and that simply may not happen. Meanwhile everyone’s plans have been delayed by weeks, and the buyer’s are in a nightmare scenario, because they have no place to live during all of this, and the seller’s probably packed everything up in boxes and are practically moved out of the home. In addition, the sellers are also probably buyers for a home where they intend to move to, and that is means they have another pending transaction that will have to have the closing date extended, and that might not work for those sellers.

In my buyer’s transaction, the sellers did agree to reduce the price by $30,000, and everyone will be able to move on with their plans. A low appraisal is rare, but when it does happen, it is unfortunate for the sellers especially. The practical solution in most cases of a low appraisal is for the sellers to agree to reduce the price. There are exceptions to this rule, but those exceptions are as rare as the low appraisal itself.

Last Updated on September 6, 2019 by Chuck Marunde

I purchased a home in Sequim in 2014, and my lender was Wells Fargo, of Vacaville. The lender set up a appraisal who was not from the peninsula and his appraisal was $40,000 lower then the asking price. And the seller believed his home was priced correctly and refused to lower his price. The seller also was here to meet with the appraiser and knew he was not familiar with this area. I know , that should not matter, due to comps and other factors.

After speaking to the seller I hired a lender from Sequim, they used a local appraiser and the new appraisal was $30,000 over asking price.

I lost my faith in the whole process, but I am happy my house closed with only a 30 day delay. It was a stressful expierance. In 2012 I had finished all college courses needed to be a licensed Ca. realastate appraiser. Way too much for me to pursue as a hobby job.